Interrupted Time Series (ITS) with scikit-learn models#

This notebook shows an example of using interrupted time series, where we do not have untreated control units of a similar nature to the treated unit and we just have a single time series of observations and the predictor variables are simply time and month.

import pandas as pd

from sklearn.linear_model import LinearRegression

import causalpy as cp

%config InlineBackend.figure_format = 'retina'

Load data#

df = (

cp.load_data("its")

.assign(date=lambda x: pd.to_datetime(x["date"]))

.set_index("date")

)

treatment_time = pd.to_datetime("2017-01-01")

df.head()

| month | year | t | y | |

|---|---|---|---|---|

| date | ||||

| 2010-01-31 | 1 | 2010 | 0 | 25.058186 |

| 2010-02-28 | 2 | 2010 | 1 | 27.189812 |

| 2010-03-31 | 3 | 2010 | 2 | 26.487551 |

| 2010-04-30 | 4 | 2010 | 3 | 31.241716 |

| 2010-05-31 | 5 | 2010 | 4 | 40.753973 |

Run the analysis#

result = cp.InterruptedTimeSeries(

df,

treatment_time,

formula="y ~ 1 + t + C(month)",

model=LinearRegression(),

)

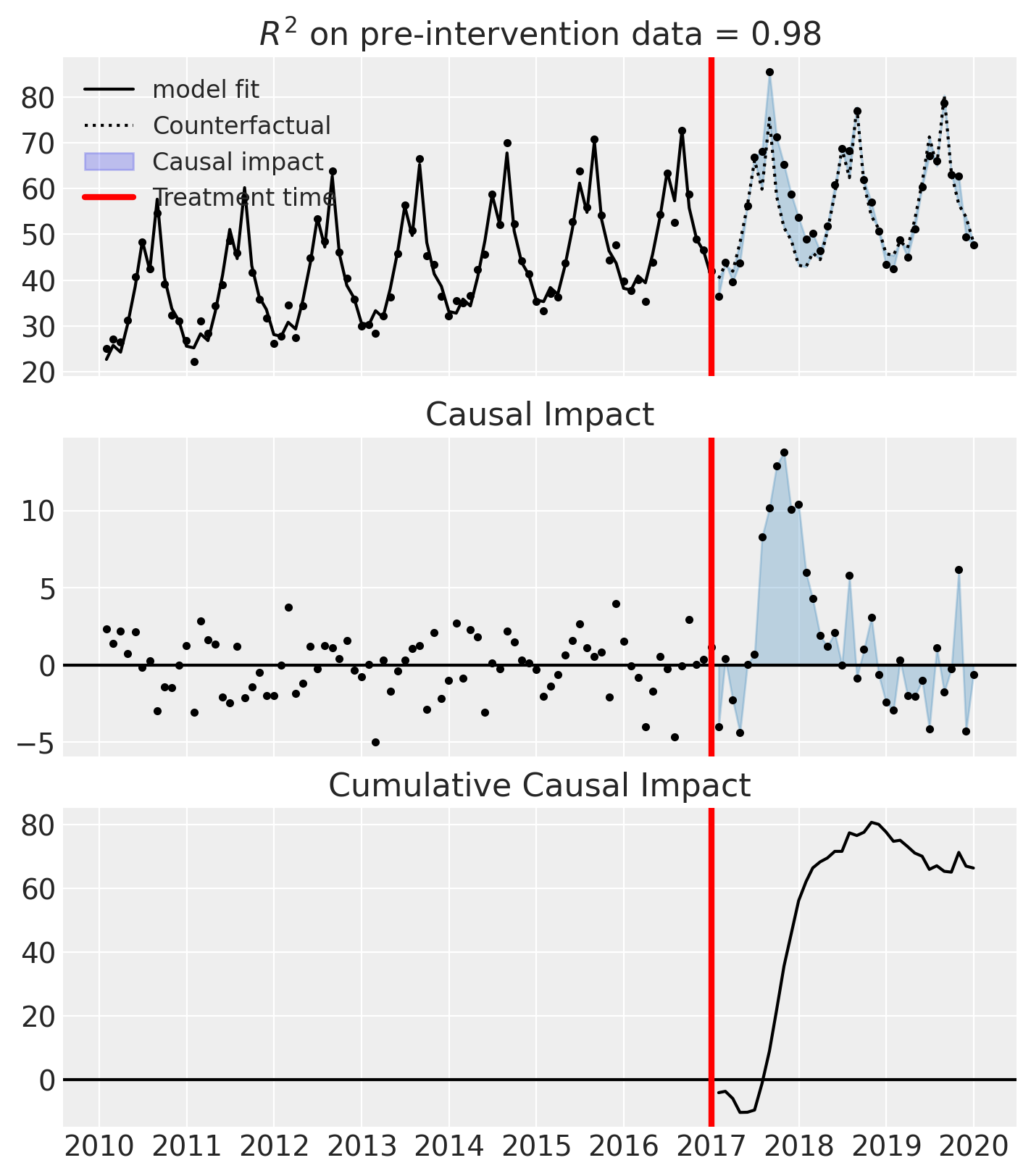

Examine the results#

fig, ax = result.plot()

result.summary(round_to=3)

==================================Pre-Post Fit==================================

Formula: y ~ 1 + t + C(month)

Model coefficients:

Intercept 0

C(month)[T.2] 2.85

C(month)[T.3] 1.16

C(month)[T.4] 7.15

C(month)[T.5] 15

C(month)[T.6] 24.8

C(month)[T.7] 18.2

C(month)[T.8] 33.5

C(month)[T.9] 16.2

C(month)[T.10] 9.19

C(month)[T.11] 6.28

C(month)[T.12] 0.578

t 0.21

Effect Summary Reporting#

For decision-making, you often need a concise summary of the causal effect. The effect_summary() method provides a decision-ready report with key statistics.

Note

OLS vs PyMC Models: When using OLS models (scikit-learn), the effect_summary() provides confidence intervals and p-values (frequentist inference), rather than the posterior distributions, HDI intervals, and tail probabilities provided by PyMC models (Bayesian inference). OLS tables include: mean, CI_lower, CI_upper, and p_value, but do not include median, tail probabilities (P(effect>0)), or ROPE probabilities.

# Generate effect summary for the full post-period

stats = result.effect_summary()

stats.table

| mean | ci_lower | ci_upper | p_value | relative_mean | relative_ci_lower | relative_ci_upper | |

|---|---|---|---|---|---|---|---|

| average | 1.845561 | 0.161437 | 3.529686 | 0.032645 | 3.366709 | 0.150601 | 6.582817 |

| cumulative | 66.440209 | 5.811718 | 127.068701 | 0.032645 | 121.201506 | 5.421618 | 236.981394 |

# View the prose summary

print(stats.text)

Post-period (2017-01-31 00:00:00 to 2019-12-31 00:00:00), the average effect was 1.85 (95% CI [0.16, 3.53]), with a p-value of 0.033. The cumulative effect was 66.44 (95% CI [5.81, 127.07]); p-value 0.033. Relative to the counterfactual, this equals 3.37% on average (95% CI [0.15%, 6.58%]).